.jpg)

Alpine Capital Investor Newsletter - Q1 2026

Share article

1. Market overview and state of the economy

Q1 was humbling for headline index watchers. The S&P 500 closed down 4.8% — its second consecutive negative first quarter — and the Nasdaq 100 fared slightly worse at –5.8%. Globally the picture was more measured: the MSCI World Index finished the quarter at –3.1%, the MSCI All Country World Index at –3.1%, and the MSCI Emerging Markets Index essentially flat at –0.1%. The equal-weighted S&P 500 also eked out a small gain — a meaningful signal in itself. For much of the past two years, returns in the US market had been driven almost entirely by a handful of large technology companies, while the average stock was left behind. In Q1, that changed: a far wider range of companies across different industries participated in the market's performance, rather than the index being carried by a small group at the top.

The quarter was defined by two collisions. The first was one we had been expecting: the market's sudden recognition that AI agents pose a genuine threat to the mainstream business software layer, accelerating after late-January product launches from Anthropic and culminating in a repricing that wiped approximately two trillion dollars from Software as a Service (SaaS) companies in a matter of weeks. The second was one no investor could have priced — direct hostilities between the US and Iran on 28 February, the closure of the Strait of Hormuz, and Brent crude's surge through $100 for the first time since 2022, finishing the quarter over $110 (up more than 85% YTD). The energy shock was material, but historically these episodes are shorter-lived than the headlines suggest. Emergency inventory releases, OPEC+ spare capacity utilisation and the US's relative energy independence have already begun to cushion the impact. The American economy enters this shock from underlying strength rather than fragility.

Three data points paint a picture of an economy in genuinely good health: manufacturing expansion, services expansion, and accelerating corporate earnings.

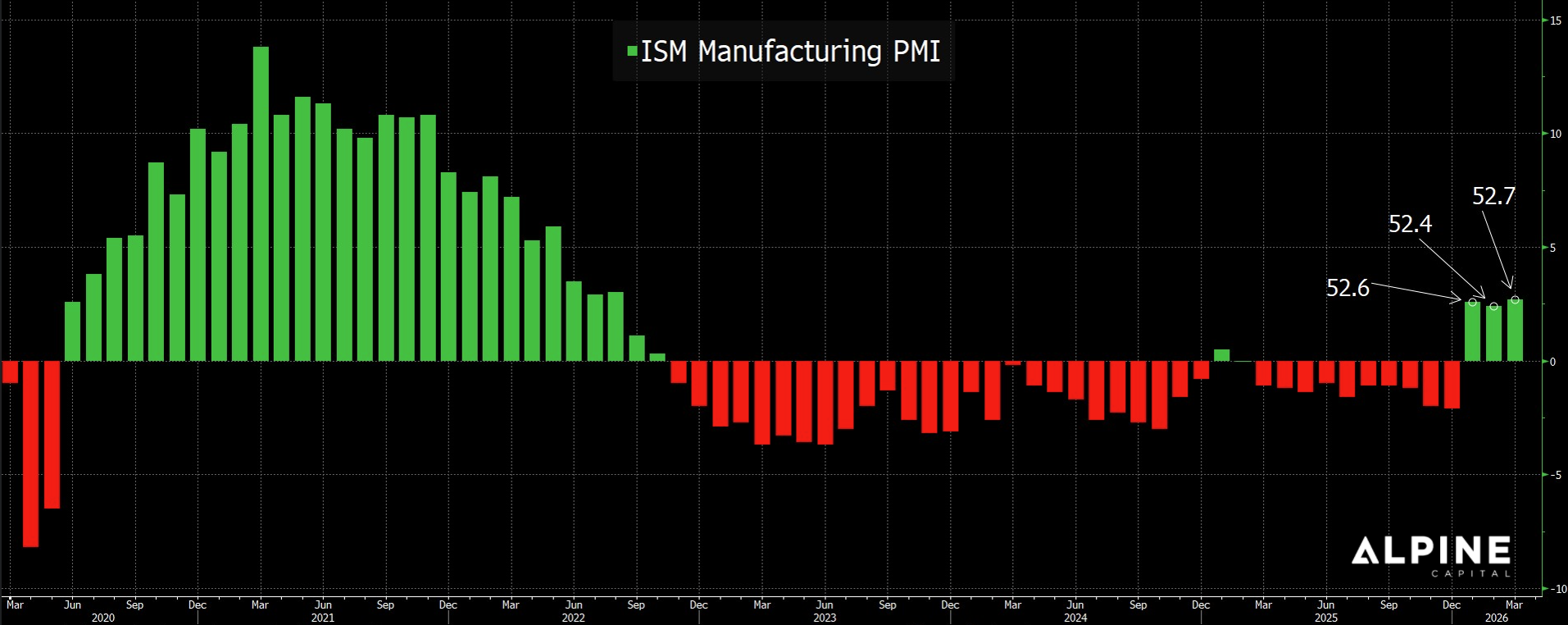

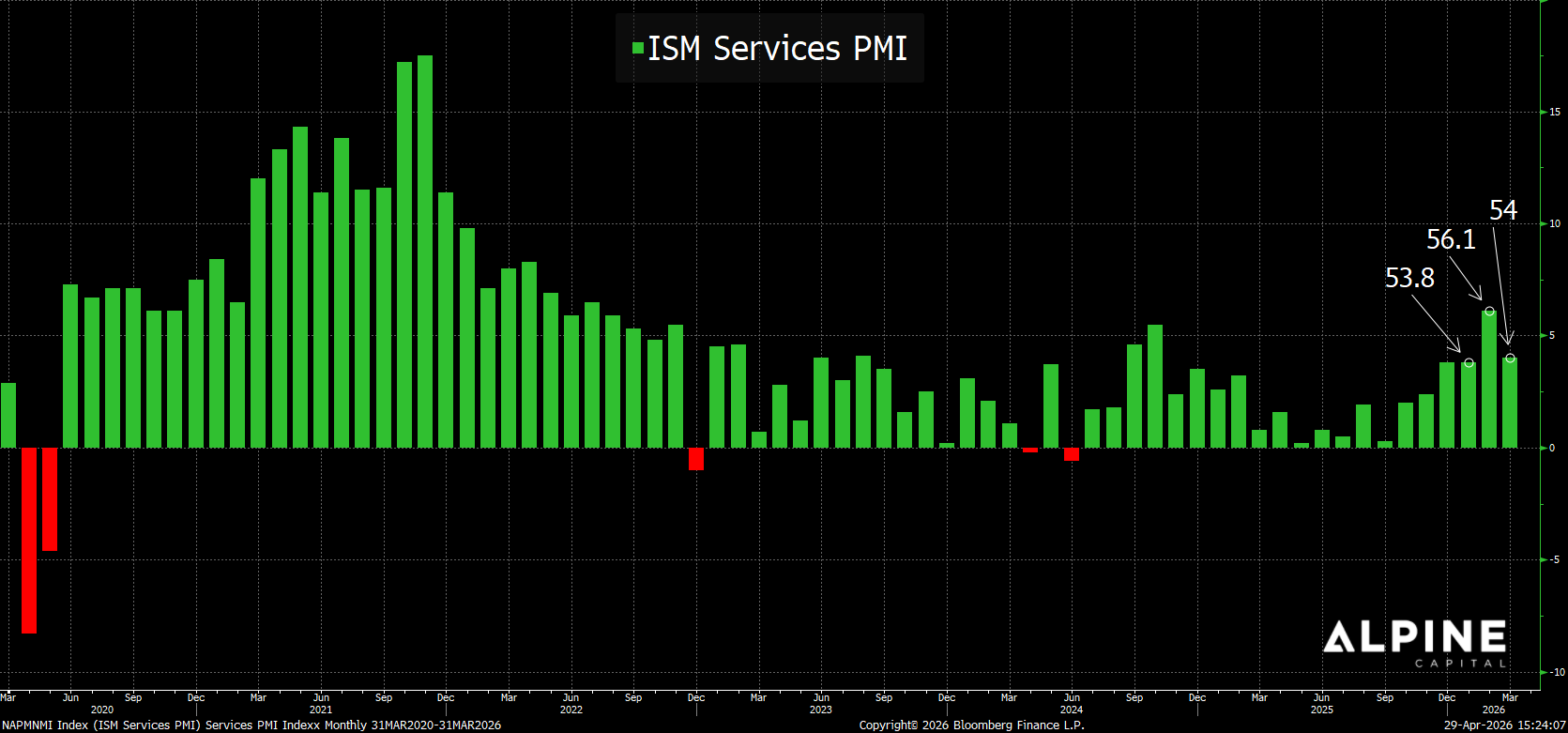

The ISM Manufacturing PMI, which we flagged in Q4, posted three consecutive expansionary readings — 52.6, 52.4, and 52.7 — the strongest since August 2022 and the first three-month expansion in forty months. Equally important, and less widely discussed, the ISM Services PMI told the same story on the other side of the economy: 53.8 in January, accelerating sharply to 56.1 in February — the strongest reading since July 2022 — before settling at 54.0 in March, its 21st consecutive month in expansion territory. It is worth reminding clients what services represent: roughly 70% of the US economy. When both manufacturing and services are simultaneously expanding at multi-year highs, it is as close to a clean bill of health as an economy can produce.

From a company earnings perspective, the S&P 500 is on track to report earnings growth of 13.2% for Q1 — the sixth consecutive quarter in which corporate profits have grown by double digits. What makes this particularly noteworthy is that analysts have been upgrading their expectations throughout the quarter, revising the full-year 2026 earnings growth forecast upward from 15% at the start of the year to approximately 17.4% by quarter-end. In other words, companies are not just meeting expectations — they are consistently beating them, prompting analysts to raise the bar. That kind of upward revision mid-quarter is unusual and is a strong signal of the underlying health of corporate America.

2. The "SaaSpocalypse" and the commoditisation of software

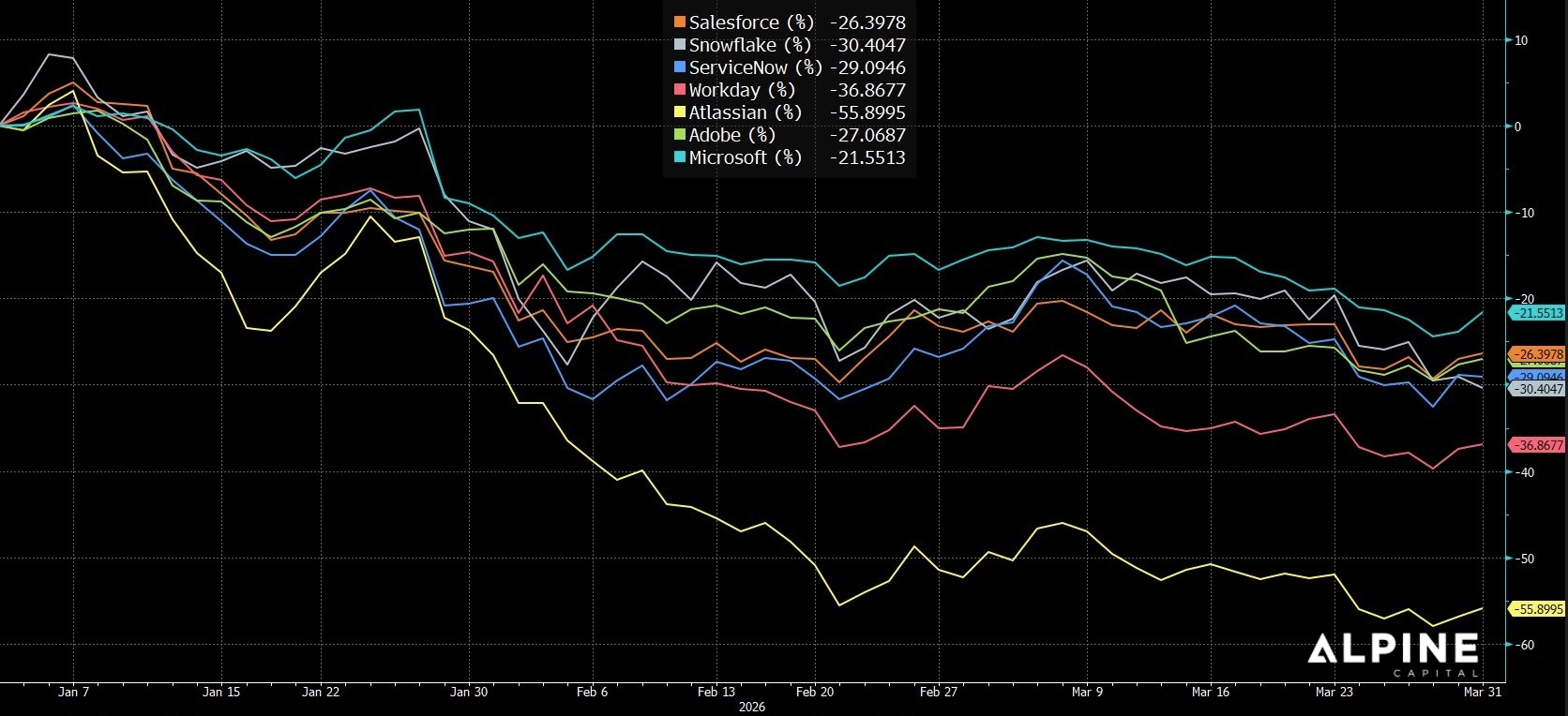

In Q4 we flipped our stance on software incumbents from constructive to neutral/bearish, arguing that if a proprietary application that once cost $5 million to develop could now be replicated for $5,000, the competitive advantage of owning that software could begin to evaporate. We did not expect the thesis to be stress-tested so rapidly. The iShares Expanded Tech-Software Sector ETF (IGV) finished the quarter down roughly 24% — its worst quarterly performance since 2008. The financial press has coined a name for it: the "SaaSpocalypse."

The catalyst was a product launch, not a macro shock. Anthropic's late-January release of Claude Cowork, combined with the rapid maturation of Claude Code and competing agentic offerings from OpenAI and Google, forced investors to confront a question they had been avoiding: if an AI agent can perform the work of ten human users at a fraction of the cost, why would an enterprise pay for ten per-seat SaaS licences? Salesforce, Snowflake, ServiceNow, Workday, Atlassian and Adobe were all sold heavily. Atlassian reported its first-ever decline in enterprise seat counts. Even gigantic Microsoft was not immune to the sell-off.

It is important to be specific about where the threat sits. Our concern is concentrated on what is known as the horizontal software layer — software built to handle one general-purpose workflow (managing customer relationships, processing payroll, logging IT tickets) and sold as essentially the same product to every industry, from law firms to retailers to manufacturers. This layer commanded premium multiples for a decade because the model appeared close to ideal: high margins, recurring revenue, and a vast addressable market that could be served by a single standardised product. AI challenges every one of those assumptions simultaneously, because a standardised workflow is exactly the kind of task an AI agent can now replicate. Roughly 70% of listed software providers acknowledge that the cost of delivering AI features is eroding gross margins. The terminal value of many of these businesses has genuinely been cut in half, and we do not think the market is wrong in having repriced them. Vertical software — purpose-built for a specific industry, such as radiology imaging, mining operations or air traffic control — is far less exposed, because the deep domain knowledge embedded in those products is much harder for a general-purpose AI agent to replicate.

That said, parts of the sell-off have been indiscriminate, and it is here that we want to draw an important distinction. The businesses genuinely under threat are commercial software tools — products people use because their employer pays for them and would readily replace if something cheaper did the same job. What is categorically different are the centralised ecosystems that billions of people come to voluntarily, every single day, for reasons that go far beyond work. Meta, Alphabet and Amazon do not sell a workflow tool that a CFO can cancel in a budget review. They own the digital real estate where people communicate, search, shop, watch, and increasingly live their digital lives. No AI agent can displace that. If anything, AI strengthens their position — every new AI feature, every new agent, every new capability gets deployed through platforms that already have the users, the data, and the daily habit. These companies’ moats are not under attack. They are the centralised infrastructure of modern life, and that is a position AI reinforces rather than threatens. Microsoft sits in a more complicated position given its deeper exposure to commercial productivity software, but it owns the operating system that runs the world's computers, the login system that controls access to most corporate environments, and the cloud infrastructure that an enormous share of global business depends on. We believe it weathers this storm.

3. AI 2.0 update: power, state bans, and the CPU re-awakening

Memory, power, semiconductor equipment and industrial metals have emerged as the real choke points on the AI buildout. Memory stocks were the standout trade, with HBM (High Bandwidth Memory) capacity for 2026 now fully allocated under binding multi-year contracts — an unusual level of forward revenue visibility for an industry historically defined by commodity cyclicality.

To understand why we are so focused on this theme, it helps to separate the demand side from the supply side — because both are moving in the same direction simultaneously. We are of the opinion that the market is not fully pricing in these mechanics at work.

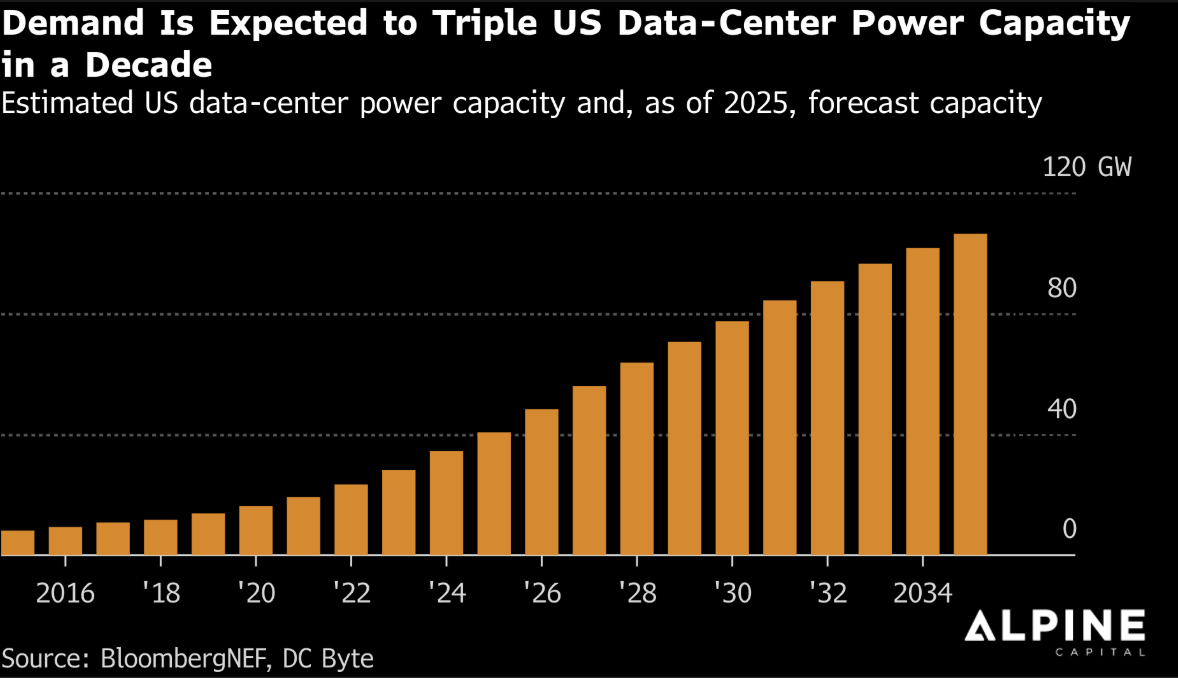

On the demand side, the scale of what is being built is still being underestimated. Power demand from US data centres alone is projected to reach 106 gigawatts by 2035 — a figure that was revised upward by roughly 36% in the space of just seven months. That kind of upward revision, at that speed, tells you that even the people analysing and closest to this buildout are consistently underestimating the demand. Every new AI model released, every new agentic product launched, every enterprise that moves from pilot to full deployment adds another layer of demand onto a grid that was never designed to carry it. The demand pressure is real, it is accelerating, and it is not fully appreciated.

On the supply side, the picture is becoming actively more constrained — and this is the part of the story that is most under-appreciated, in our view. The world already had a serious shortage of power-approved data centre capacity before regulators got involved. Now supply is being throttled from the top down. As of the end of Q1, at least twelve US states had filed legislation imposing formal moratoriums on new data-centre construction. Community groups have separately blocked or delayed over $60 billion of announced projects in the past year alone. Residential electricity bills in states such as Maine and Virginia have moved sharply higher, and the political backlash is real — it has cross-party support and it is not going away. This is not a technical or financial constraint that can be solved by spending more money. It is a political constraint, and political constraints are the slowest kind to resolve.

The consequence of demand accelerating while supply is being throttled is straightforward: existing approved power and data-centre capacity becomes dramatically more valuable, interconnection queues lengthen further, and the timeline for new capacity stretches from years to potentially a decade in the most constrained markets. Put simply, you have a demand story that the market is already underestimating, colliding with a supply story that the market has barely begun to price. That collision is the investment thesis, and it is one we have been positioned for since Q2 last year. Our portfolios carry substantial exposure to companies operating across the data-centre and energy value chain — power generation, grid infrastructure, cooling, semiconductor equipment and industrial metals — and given the demand-supply dynamics described above, we are actively considering adding to that exposure from here.

4. What we acted on in Q1

This section refers specifically to activity within our Global Active portfolio.

We made a number of deliberate moves during Q1 to align positioning with the views we laid out in Q4. On the buy side, we added the Global X Copper Miners ETF (COPX) to capture the industrial-metals leg of the AI physical-buildout thesis, initiated a position in Exxon Mobil and moved overweight energy to provide a hedge against Middle East volatility, and initiated a position in AMD.

On the sell side, we exited the iShares Expanded Tech-Software Sector ETF (IGV), the First Trust Cybersecurity ETF (CIBR) and the iShares US Medical Devices ETF (IHI). The CIBR and IHI sales do not reflect a structural view on either sector; we continue to regard cybersecurity and medical devices as attractive long-term themes. Both were portfolio-management decisions to make room for new positions and manage concentration.

Laggards we still believe in. Galaxy Digital has disappointed despite a thesis that only strengthened through Q1; it remains miscategorised as crypto-adjacent and has been caught in the broader Bitcoin drawdown. Bitcoin closed Q1 down approximately 24% at around $67,000, weighed down by three factors: the quantum-computing threat moving from theoretical to a live debate after Caltech and Google research papers in March; capital rotating out of digital assets into anything AI-related; and the stalled Clarity Act holding back institutional flows. None is permanent. Amazon has lagged the other Magnificent Seven on AWS (Amazon Web Services) deceleration concerns and software-exposure fears — in our view overdone. The alternative-asset managers — Apollo, Brookfield and KKR — were caught in the software-related private-credit scare, but actual software exposure within their books is small relative to portfolios that skew heavily toward infrastructure, real estate and energy. The sell-off has created an opportunity.

Berkshire Hathaway and the handover. Warren Buffett stepped down as CEO on 1 January after sixty years, with Greg Abel taking over. We continue to hold Berkshire — not because we expect it to wildly outperform, but because its capital discipline, low turnover and willingness to sit on cash when nothing looks attractive remain valuable from a portfolio-management perspective. We also believe the transition could spark renewed action, and there are already signs. Abel closed the $9.7 billion OxyChem acquisition on 2 January, resumed share repurchases on 4 March for the first time since May 2024, personally purchased roughly $15 million of Berkshire stock, and committed his entire after-tax salary to Berkshire shares. A new CEO with sixty years of predecessor to live up to will want to make his mark early — and the $380-plus billion cash pile is the tool with which he will do it.

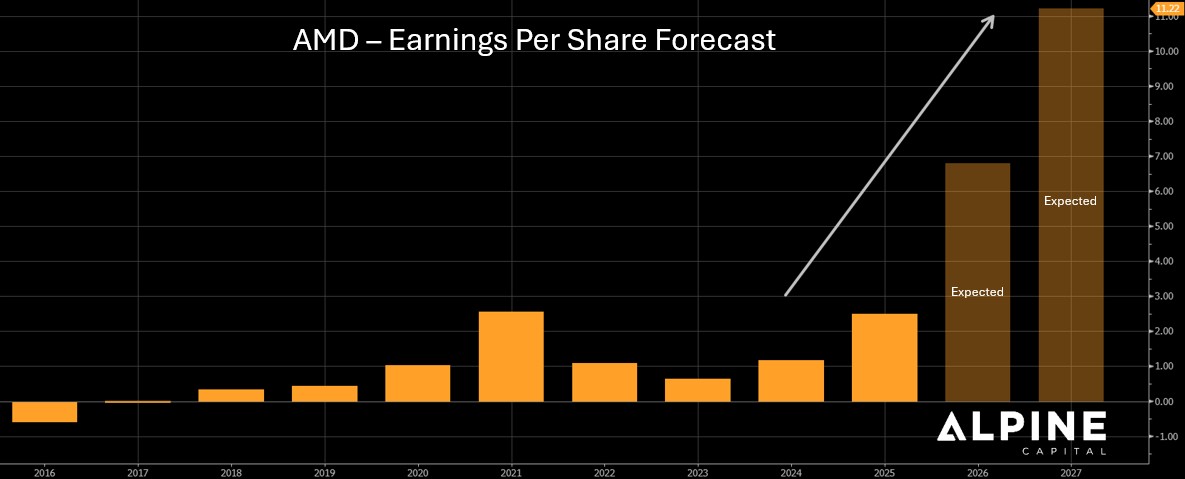

AMD — why we bought it. To understand the thesis, it helps to know the difference between a GPU and a CPU. A CPU (Central Processing Unit) is the general-purpose brain of any computer — the chip inside every laptop, phone, server and everyday device that handles the broad range of tasks a machine needs to perform. A GPU (Graphics Processing Unit) was originally designed to render images and video, but it turned out to be extraordinarily good at the kind of massive parallel computation that training AI models requires. Think of a CPU as a highly skilled manager who can handle any task, and a GPU as a warehouse full of workers who can all do the same repetitive task simultaneously at enormous speed.

The AI compute story has unfolded in two stages so far. Stage one was training the AI models themselves — teaching the system everything it knows — which required vast numbers of GPUs running simultaneously. This was almost entirely an Nvidia story. Stage two was inference at the enterprise and hyperscaler level — the process of actually using those trained models to answer questions and perform tasks at scale for large corporations and cloud providers. This broadened the winners to include AMD, the memory suppliers and the semiconductor-equipment makers.

Stage three is now beginning, and this is why we bought AMD. Stage three is the deployment of AI to ordinary people and to small and medium-sized businesses — the phase where AI stops being a tool for large corporations and data scientists and becomes part of everyday life. A person using AI on their laptop, a small business running an AI assistant, a mid-sized company deploying AI across its operations — none of these run on expensive GPU clusters. They run on the CPUs already embedded in the devices they own. This is an inherently CPU-heavy phase of the AI rollout. When demand rises faster than supply, two things tend to happen at the same time: more units get sold, and the price of each unit goes up. For AMD, that means potentially selling more chips at higher prices simultaneously — a combination that can be very powerful for earnings and ultimately for the share price.

5. South Africa and emerging markets

South African and emerging-market equities have had a remarkable run, and we do not expect that to simply reverse — but we equally do not expect a repeat of 2025's exceptional returns. Our base case is that these markets broadly keep pace with global peers from here, rather than dramatically outperforming or underperforming.

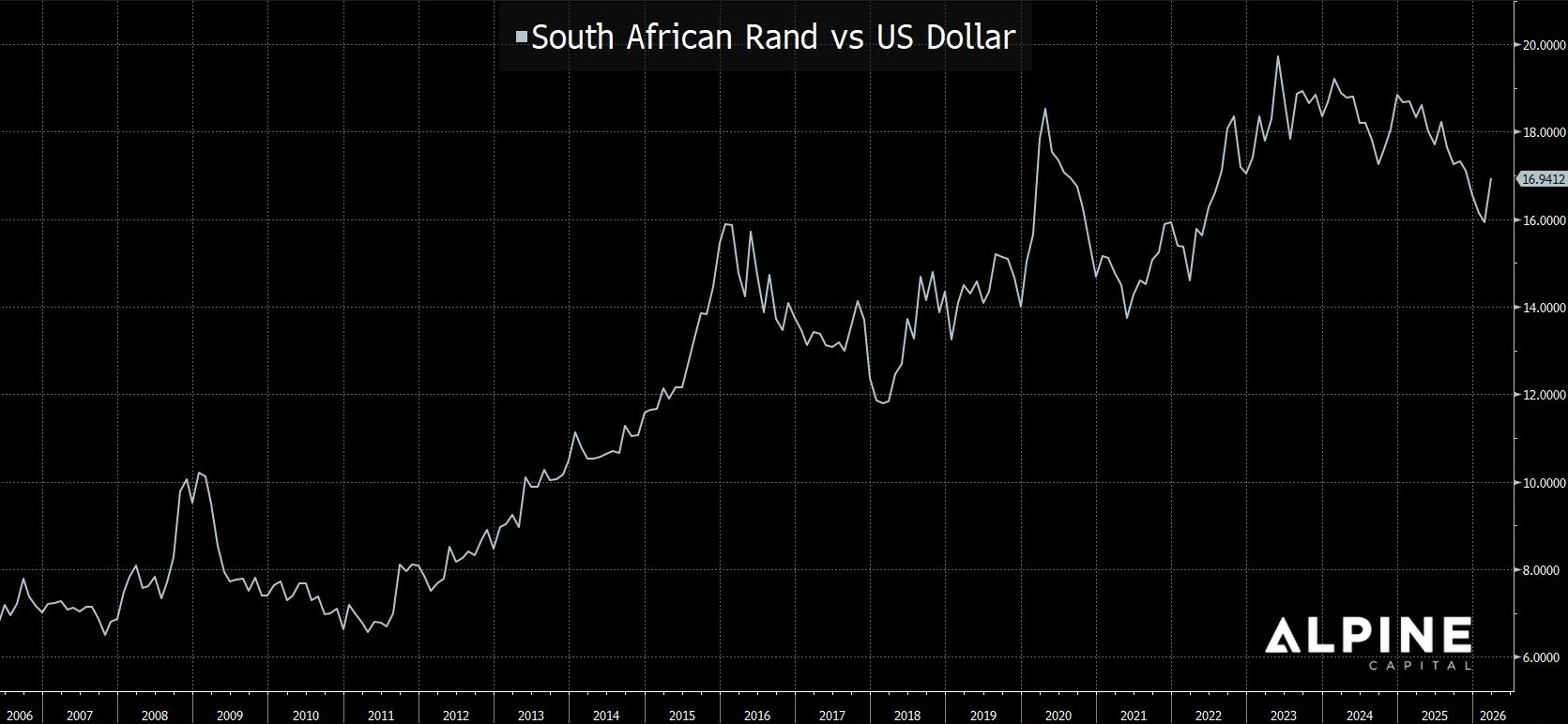

The currency tells an important part of the story. The rand strengthened sharply to roughly R15.70 against the dollar by late January — a level that already reflected a great deal of good news — before giving back nearly all of those gains as the Iran war unsettled risk sentiment globally, closing the quarter above R17.00. In our view the Rand is now closer to a floor than a ceiling.

What keeps us comfortable holding our South African positions is the combination of genuinely attractive income, portfolio diversification, and selective opportunities in individual companies that we believe are undervalued on their own merits. The commodity complex continues to provide a structural tailwind — gold and platinum in particular have benefited from the drivers we have been writing about since Q3 2025, with the Iran war adding a fresh layer of support. We are not chasing South African equities for index outperformance. We are holding them because the underlying businesses make sense, the income is real, and the commodity tailwind remains intact.

6. Outlook

We enter the second quarter cautiously optimistic, but with humility — the macro picture has more moving parts than at any point in the past eighteen months. Our base case is that the Iran war fades as a market-moving event over the coming months, and equities have already begun to price this in. We are not overly concerned about inflation at this stage — our base case remains that the disinflationary trend stays broadly intact. That said, we are watching it closely. The oil spike fed directly into the ISM Prices Index, which jumped to 78.3 in March from 59 in January, and energy cost pass-through typically shows up in CPI and PCE prints with a one-to-two-month lag. The next several inflation readings may disappoint on the upside, and we are monitoring whether this proves transitory or begins to show signs of something more persistent. For now, we believe it is the former.

That picture runs into the most consequential macro appointment of the year: the Federal Reserve chair succession. Jerome Powell's term ends in May, and in late January the administration nominated Kevin Warsh as his successor. Assuming Warsh is confirmed — which we treat as the base case though not a certainty — he inherits a delicate balancing act. He will face significant political pressure to lower the Fed Funds rate, and in a world where inflation remains broadly under control, that path is achievable. The near-term inflation noise from the oil shock complicates the timing, but does not change the direction. For our clients, the practical risk in 2026 is not the direction of rates but the uncertainty around the path — which argues for shorter duration on the fixed-income side and for owning businesses with genuine pricing power on the equity side.

We close with a thought from Howard Marks — the billionaire co-founder of Oaktree Capital and one of the most respected voices in global investing, known for his decades of writing on market cycles, risk and investor psychology. Marks is particularly worth listening to here because he has been on a very public journey with AI. For much of 2024 and into 2025 he was openly sceptical, cautioning that AI had many of the hallmarks of a speculative bubble and that investors were getting ahead of themselves. Then, earlier this year, after spending considerable time interacting with the latest frontier models himself, he changed his mind — publicly and explicitly. Having experienced the technology firsthand, he concluded that AI is not a search engine or an incremental productivity tool, but a system genuinely capable of reasoning, synthesising and executing work in ways that will reshape the global economy. His revised framing captured our own positioning better than we could: "No one should go all-in... but no one should stay all-out." His point was simple — the risk of ruin from over-committing is real, but so is the risk of missing one of the great technological steps forward by disengaging entirely. We find ourselves in exactly that position — clear-eyed about the risks, but unwilling to step away from an opportunity set we believe is genuinely attractive. The market is not cheap, geopolitical uncertainty is elevated, and the Fed succession is unresolved. But beneath that noise, the underlying businesses we own are compounding, earnings are growing, and the structural drivers we have been writing about remain firmly in place. You cannot make money by sitting on the sidelines. You must participate in the race — and we intend to do so with conviction, discipline and a clear understanding of what we own and why.