Alpine Capital Investor Newsletter - Q2 2025

Share article

1. Market Overview and Performance

The second quarter of 2025 began with significant market turbulence, sparked by the US administration’s abrupt “Liberation Day” announcement of broad tariffs on most global trading partners. This triggered a sharp sell-off in global equities in April, as investors grappled with heightened uncertainty. However, on April 9, President Trump’s decision to pause these tariffs for 90 days catalysed a robust market recovery, bolstered by subsequent progress in trade negotiations with key partners. This shift restored investor confidence, enabling markets to stabilise and rebound.

The second quarter saw the MSCI All Country World Index and MSCI World Index both gaining 11.5% in USD terms, driven by strong performances in US markets. The tech-heavy NASDAQ surged 18.0%, fuelled by exceptional corporate earnings in technology and artificial intelligence (AI) sectors, while the S&P 500 delivered a solid 10.9% return, outpacing most global peers. Emerging markets also performed well, with the MSCI Emerging Markets Index rising 12.0%, and South Africa’s FTSE/JSE All Share Index climbing 14.0% in USD terms.

In our Q1 letter, we cautioned against overreacting to rapid policy shifts, emphasising the American economy’s underlying strength despite short-term disruptions. This perspective proved prescient. Our decision to maintain steady portfolio allocations, rather than chasing tactical repositioning, allowed us to capture the market rebound following the tariff pause. While volatility and headlines might have suggested aggressive adjustments, such moves would likely have led to underperformance given the swift recovery. The market’s ability to absorb tariff-related concerns, coupled with minimal inflationary impact and advancing trade talks, suggests investors are increasingly viewing these disruptions as transient. With President Trump’s political capital on trade issues waning, a pragmatic resolution appears likely, further supporting market stability.

2. US Dollar, South Africa, and ZAR

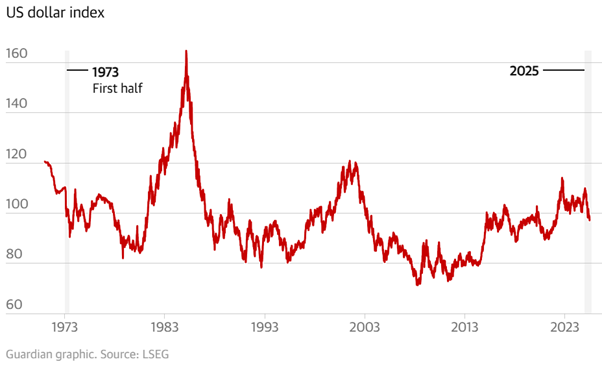

The US dollar experienced significant pressure in 2025, declining 10.8% against a basket of currencies in the first half of the year—its weakest first six-month performance since 1973. While further USD softness is possible, we believe the majority of this correction is behind us. Interest rate differentials and improving global trade dynamics should support dollar stabilisation in the near term. Alarmist narratives about the “end of the dollar” are overstated; historical cycles show such weakness is not uncommon, and the USD remains a cornerstone of global finance.

The South African Rand (ZAR) struggled to fully capitalise on USD weakness in Q2, reflecting South Africa’s broader economic challenges. The ZAR weakened to a record R19.93 against the USD in early April amid tariff fears but recovered to R17.57 by early July, posting a 9.56% gain over the 90-day period ending in June. Despite this improvement, the ZAR failed to break below R17.50, underscoring its vulnerability to global shocks. At current levels, we see the USD/ZAR exchange rate as an attractive opportunity to acquire dollars, given the ZAR’s relative underperformance.

South Africa’s economic outlook remains constrained by the lack of a significant growth catalyst. While valuations of South African assets are compelling, a meaningful rerating of equities or the ZAR requires robust GDP expansion, which remains elusive absent structural reforms or external demand surges. Political developments are unlikely to provide the necessary impetus, and the looming risk of US tariffs on South African exports, poses an additional hurdle.

3. Portfolio Positioning and Technology Focus

Our portfolio strategy continues to emphasise technology stocks, particularly the “Magnificent 7” and other leaders poised to capitalise on the accelerating adoption of AI and digital transformation. These companies are uniquely positioned to deliver sustained revenue growth and margin expansion as AI permeates both digital and traditional economies. Our approach prioritises the future over the past, favouring innovation-driven sectors over legacy industries.

The AI revolution is reshaping markets, and we are actively identifying the next wave of transformative companies. The current Magnificent 7—global leaders with unmatched scale—remain central to our thesis, as their ability to invest in large-scale data centres and advanced AI models creates formidable barriers to entry. Consider the below table, highlighting the estimated capital expenditures earmarked for 2025.

.png)

Source: Alpine Capital Research

To put things in perspective, consider the following statistics:

- The Magnificent 7’s $330.7billion Capex is larger than the market capitalisation of approximately 440 out of ~500 S&P 500 companies (88%)

- Amazon’s $100 billion Capex alone exceeds the market cap of 80% of S&P 500 companies, including firms like Ford ($30B), General Motors ($55B), and Target ($75B), based on mid-2025 estimates.

These firms leverage their size and integrated ecosystems to drive efficiencies, expand market share, and widen their competitive moats, positioning them to dominate future growth.

Salesforce CEO Marc Benioff recently highlighted AI’s transformative role, noting that it currently handles 30% – 50% of critical functions such as engineering, coding, support, and customer service at Salesforce, with expectations of further expansion. Similarly, Amazon CEO Andy Jassy emphasised AI’s impact in a recent letter, stating, “…we anticipate a reduction in our corporate workforce as AI-driven efficiencies are implemented across our operations.” These insights underscore a clear reality: AI is not a distant promise but a present force.

However, we are closely monitoring potential disruptions, particularly in the software-as-a-service (SaaS) sector. Over the next few years, SaaS companies could face risks of obsolescence unless they adapt, presenting both challenges and opportunities for investors.

A key opportunity is emerging from the rising electricity demand driven by AI's energy needs. The US's outdated infrastructure requires upgrades to sustain its AI leadership, opening investment potential in utilities and related sectors. Consequently, we’ve added Galaxy Digital Holdings—a digital asset and AI infrastructure-focused company—to select portfolios, seeing it as an asymmetric investment opportunity. The investment centres on its Helios data infrastructure facility in West Texas, which has shifted from Bitcoin mining to AI use, leveraging 800MW of approved ERCOT power to avoid 36-month delays, with an additional 1.7GW (totalling 2.5GW) in progress to meet growing AI demand. A recent deal with CoreWeave for the initial 600MW ensures strong cash flow and stability. Effective management execution could deliver substantial returns over the next 2–3 years, though volatility is anticipated in the coming months.

We capitalised on attractive valuations in the semiconductor sector by initiating a position in Lam Research Corporation, a premier semiconductor equipment manufacturer. Lam Research drives technological advancement by producing the machinery essential for semiconductor fabrication, positioning it as a vital enabler of the industry’s growth, akin to a modern utility. This addition strengthens our exposure to the semiconductor ecosystem while aligning with our focus on innovative, high-quality businesses.

We sold our stake in Micron Technology, a standout S&P 500 performer in 2025,as its rapid price surge drove valuations above our comfort levels. To maintain our positive outlook on the semiconductor sector, we reallocated the proceeds to the iShares Semiconductor ETF (SOXX), ensuring diversified exposure. Our initial investment in Micron was a calculated move, capitalising on its significant decline from prior highs while recognising its strong long-term fundamentals and competitive advantage.

We also exited our position in Visa, a company we’ve long respected for its formidable moat, high margins, low capital intensity, and near-duopolistic control of global card payments alongside Mastercard. However, growing concerns about potential disruption from digital assets and blockchain technology prompted us to reassess its outlook. While Visa remains a fundamentally strong business, we believe its market is vulnerable to competitive pressures that could lead to a significant valuation derating or extended period of stagnation.

One challenge we’re currently facing is the conventional sector classifications, which often fail to capture the cross-industry impact of modern companies. For example, companies like Amazon span e-commerce, cloud computing, and media, yet are confined to the “Consumer Discretionary” sector. This rigidity distorts true sector valuations and limits opportunities, which we’re currently rejecting as the correct status quo.

4. Outlook

The Federal Reserve is under considerable political pressure to lower interest rates, and consistent with historical patterns, it appears to be behind the curve. We expect rate cuts to materialise in the second half of 2025. Although inflation exceeds the Fed’s 2% target, it remains under control, and we consider the current federal funds rate excessively restrictive. This backdrop should sustain equity returns over the short to medium term, provided no unexpected external disruptions occur.

Despite persistent negative headlines, corporate feedback reflects resilience. Tariff uncertainties have slightly dampened activity, but investment in AI and productivity-enhancing technologies remains strong. While tight cost controls are softening employment figures, we see no evidence of a broader economic slowdown. The US economy is supported by tax cuts and deregulation, while Europe benefits from increased fiscal spending on defence and infrastructure.

Beyond technology leaders, we see substantial long-term potential in the broader S&P 500, where companies are leveraging AI to streamline IT systems, cut costs, and enhance margins. Our portfolio maintains a deliberate overweight in technology, driven by its global scalability and expansive market opportunities. Unlike traditional sectors, technology firms can rapidly scale client bases, fuelling exponential growth. Semiconductors remain a key overweight in our portfolios, having recovered from earlier declines. To complement our growth-focused technology investments, we continue to hold positions in banks, financial conglomerates like Berkshire Hathaway, and private equity firms such as Brookfield Corp. These holdings bolster diversification, mitigate volatility, and deliver uncorrelated returns, aligning with our innovation-driven strategy.

US valuations, while high by historical measures, are supported by AI’s structural growth and the stability of subscription-based business models prevalent in the US services sector. Looking forward, we anticipate markets will navigate policy-driven volatility with greater resilience than in the first half of 2025. Advancing trade negotiations and the fading impact of tariffs should bolster global equities, while technology’s transformative potential will drive outperformance. We remain dedicated to achieving superior returns by prioritising innovation, challenging conventional frameworks, and upholding disciplined portfolio management in a dynamic global landscape.