Alpine Capital Investor Newsletter - Q4 2025

Share article

1. Recap of 2025: The Resilience of Growth

In today's rapidly shifting market, our core investment philosophy feels more relevant than ever. We remain anchored by a single, unwavering question: “Where is the world going to?” Answering this requires a "low time preference"—the disciplined ability to look past the high-frequency noise of the daily news cycle to identify the deep, structural currents shaping the global economy.

As we reflect on the milestones of the past couple of years and look toward the horizon, we find ourselves at a historic intersection: a massive technological breakthrough is currently meeting a sobering physical reality check.

For the third consecutive year, economists and market pundits were proven wrong in their forecasts of an imminent recession. To the contrary, the second half of 2025 saw markets latch onto tailwinds from coordinated fiscal and monetary stimulus, sparking a classic "everything rally". This milestone marked the first post-pandemic year in which every major asset category posted positive returns.

However, the true narrative of 2025 was not found in digital screens, but in the explosive performance of "physical" assets. While the broader markets flourished, the Bloomberg Precious Metals Index surged by a remarkable 80.2%. Within that sector, silver emerged as the undisputed champion, delivering a staggering 136.13% (Silver Futures) gain as the world began to price in the material requirements of our new technological era.

2. AI 2.0: Global Abundance—The Shift from Software to Physicals

Our optimism regarding technology remains undiminished, but we are adapting our tactical focus to meet the next phase of development. We believe we are entering "AI 2.0"—a period in which artificial intelligence begins to foster a state of global abundance. As we have highlighted in previous newsletters, this shift will reverberate throughout the world, increasing productivity and greatly benefiting the livelihood of the general populace.

The Commoditisation of Software: A "Neutral/Bearish" Pivot

From an investment standpoint, we find it increasingly probable that software is being commoditised. For years, the path to outsized returns was paved with digital "bits," allowing investors to reap the rewards of the infinite scalability inherent in companies creating software. However, we are entering a world of software abundance that inherently threatens the competitive advantages of established tech giants.

When AI agents can write code, build applications, and automate complex workflows for a fraction of the historical cost, the "moats" of traditional Software-as-a-Service (SaaS) incumbents begin to dry up. If a proprietary application that once cost $5 million to develop can now be replicated for $5,000, the advantage of owning that software evaporates.

While these companies will adapt by creating new value for clients, the lack of a clear "safety net" makes us increasingly wary. Coupled with high valuations and a rising risk of obsolescence, we have flipped from a constructive view to a neutral/bearish stance on software incumbents.

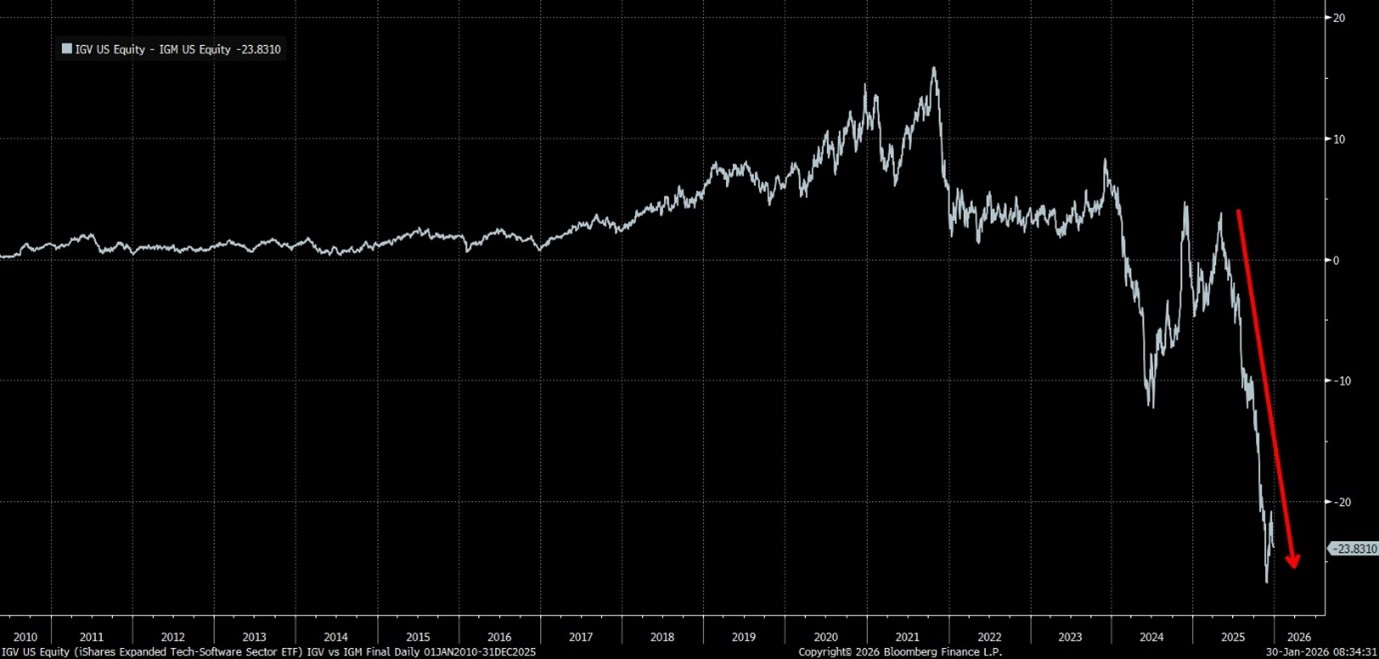

As shown above, the market has already begun to price this in. Broad tech and broad software were once highly correlated. This correlation has broken down, with software underperforming significantly. Investors think years ahead; they are placing lower multiples on these companies as their structural advantages come under attack. While "broad tech" maintains its distribution moats for now, the specialised software sector faces the most immediate threat of disruption.

So, if software “moats” are under threat, where do the opportunities lie? The primary constraints to AI advancement are no longer GPUs or CPUs—the bottleneck has shifted to the physical world.

We are witnessing a "price-inelastic" move in the hardware space. When a company builds a multi-billion-dollar "AI Factory," they do not stop construction because the price of a transformer or a kilogram of silver has doubled. They pay what is required because physical materials are now the ultimate bottleneck to digital intelligence.

As Elon Musk recently noted, "You’ve got to generate the electricity. You need transformers... you’ve got to cool the computers. Electricity generation and cooling are limiting factors for AI." This shortage is the main constraint to advancement, leading to significant data center delays and a global race for materials.

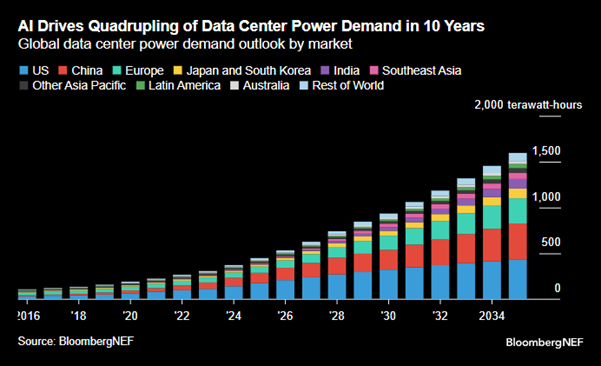

We are witnessing the birth of the "AI Factory"—massive industrial sites that function as refineries, converting raw electricity into intelligence. This global build-out is estimated to require $85 trillion over the next 15 years, necessitating an unimaginable amount of copper, silver, and power-grid infrastructure.

This is why we have seen such a violent re-rating in precious and industrial metals. We are no longer just in a digital revolution; we are in a "Re-industrialisation Revolution." Unlike the dot-com era, this is not a speculative bubble built on unproven demand; we have written about this. The compute is real, government paranoia regarding military supremacy is real, the applications are scaling, and the financing is secured.

The road to AGI (Artificial Global Intelligence) is expected to take another couple of years at best, but it doesn't end there. We are moving toward "embodied intelligence," where humanoid robots and autonomous systems redefine entire industries. As Marc Andreessen put it: "This shift is not about software eating the world; it’s about machines eating the world." The world is simply not prepared for the electricity, hardware, and commodity needs of this revolution. Consequently, we are tactically shifting our focus toward:

- The Power Chain: Companies specialising in electricity generation, thermal management, power transformers, and general infrastructure.

- Industrial Metals: Specifically, copper, which is a non-cyclical requirement for the AI grid. Copper is starting to react and is likely to follow the historic move already seen in Silver.

3. Europe and Emerging Markets: Navigating the "American Bully" and the EM Catch-Up

The surge in Emerging Markets (EM) has been a standout feature of 2025, yet it brings a complex set of questions for the long-term investor. This rally has been fuelled by a perfect storm of factors: a weakening Dollar, geopolitical shifts that sparked a massive rally in precious metals (particularly gold), and a flurry of capital forced out of the U.S. that culminated in a significant "catch-up" trade for once-depressed valuations.

We are currently grappling with the sustainability of this trend. On one hand, the Trump administration’s focus on reshoring and re-industrialisation technically favours the U.S. economy. However, the administration's aggressive "American Bully" approach to foreign policy is inadvertently driving allies and EM nations toward a unified consensus, potentially creating a new global power dynamic.

Furthermore, the AI revolution is acting as a massive funding vehicle for EM, as these nations sit on the raw materials required for what’s coming. Boatloads of cash are flowing into these regions as the global hunger for AI infrastructure is providing a structural floor for EM economies. We reiterate, however, that they are not the masters of their own fate; they are predominantly beneficiaries of prosperity created elsewhere.

Despite the attractive price action, we remain cautious. A persistent long-term impediment to investing in these regions is the ever-increasing culture of socialism, communism, and welfare, which acts as a drag on private capital. While the "Everything Rally" of 2025 lifted all boats, we believe the true long-term compounding power still resides in the world’s leading companies—the majority of which remain U.S.-listed.

4. The Federal Reserve: A Shifting Mandate and the Path to Lower Rates

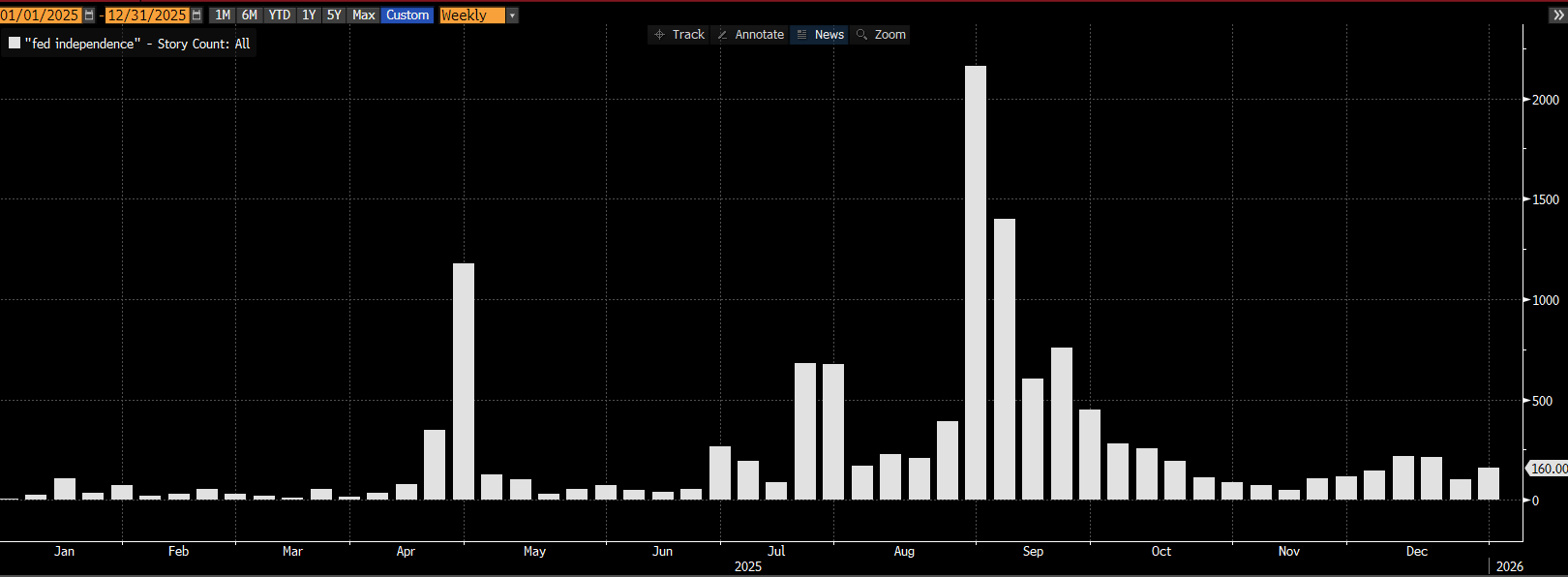

The Federal Reserve currently stands at a crossroads, navigating the difficult "dual mandate" of maintaining price stability while ensuring maximum employment. We have frequently highlighted the precarious juxtaposition the Fed finds itself in. The institutional requirement to remain independent and objective is being tested by a relentless barrage of political pressure from the Trump administration. The graph below tracks the weekly frequency of the term 'Fed independence' across all Bloomberg data sources.

As we look toward the horizon, the leadership of the Fed is entering a definitive transition phase. Chair Jerome Powell’s tenure is nearing its end, and we anticipate that his successor will be chosen specifically for their dovish leanings. Let’s not mince words: the next Fed President will undoubtedly possess an inherent bias toward lower rates—in fact, that bias is likely the primary reason for their selection. This shift paves the way for a sustained environment of accommodative monetary policy over the short to medium term.

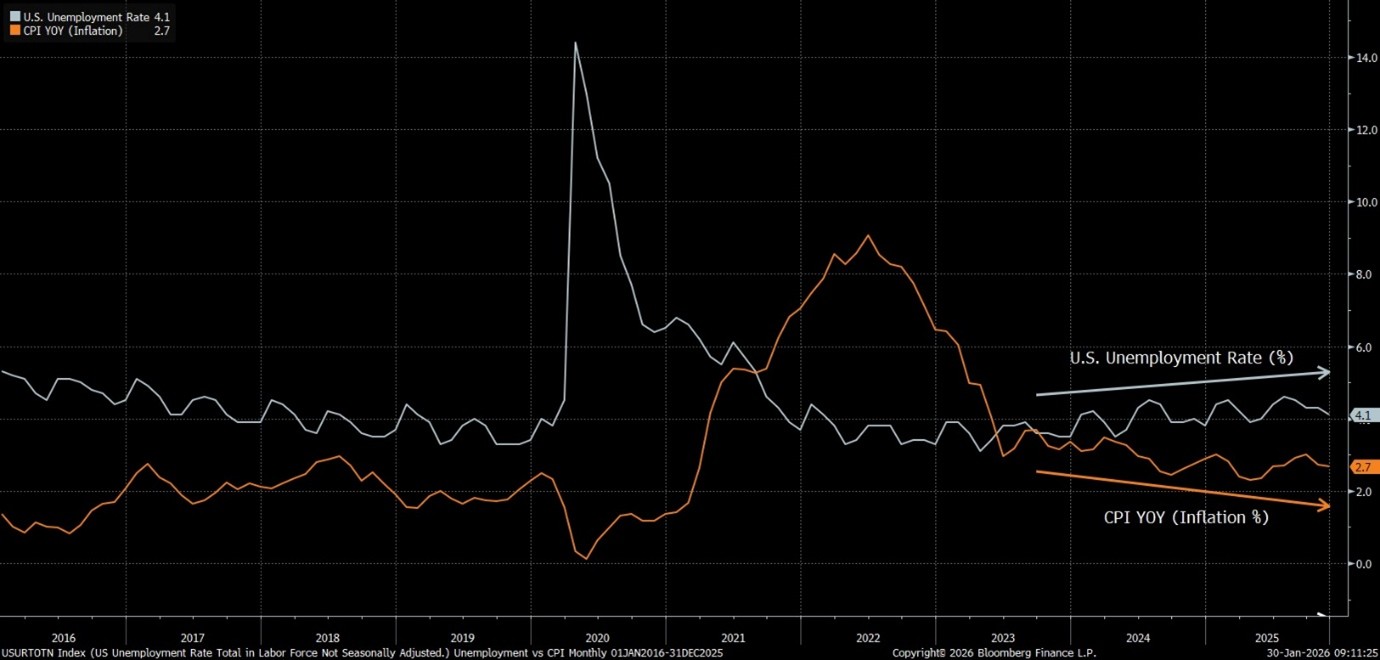

Crucially, the data suggests that inflation has stabilised and is no longer the primary threat. No one is talking about inflation anymore; the market has essentially moved on. Instead, the real challenge for the "new" Fed may lie with the labour market. We expect unemployment to face, at the very least, sustained upward pressure as AI integration accelerates across economies.

In essence, we believe the Federal Reserve will play a much smaller, less disruptive role over the coming year than it has during the high-volatility, aggressive-hiking cycles of the recent past. With a more predictable, rate-cutting bias at the helm, the central bank is likely to move into the background of the broader investment story. This, in our view, is one of the leading tailwinds for equities over the next couple of years.

5. Outlook: 2026 and the Dynamics of Mid-Term Volatility

As we look toward 2026, we remain extremely optimistic. Our conviction is supported by a robust forecast for S&P 500 earnings growth of 15%. This growth is driven by massive productivity gains as companies adopting AI see their proficiency compound.

While the long-term structural tailwinds are strong, we must prepare for an environment dominated by "high time preference" noise. 2026 is a mid-term election year, a period historically characterised by heightened volatility and subdued returns. We anticipate the White House may strategically retrace some of its more aggressive economic and foreign policy proposals to avoid losing seats.

Despite high valuations, the strength of corporate earnings provides a vital counterweight. At worst, we expect the S&P 500 to consolidate sideways; at best, it could match the 15% earnings growth expected.

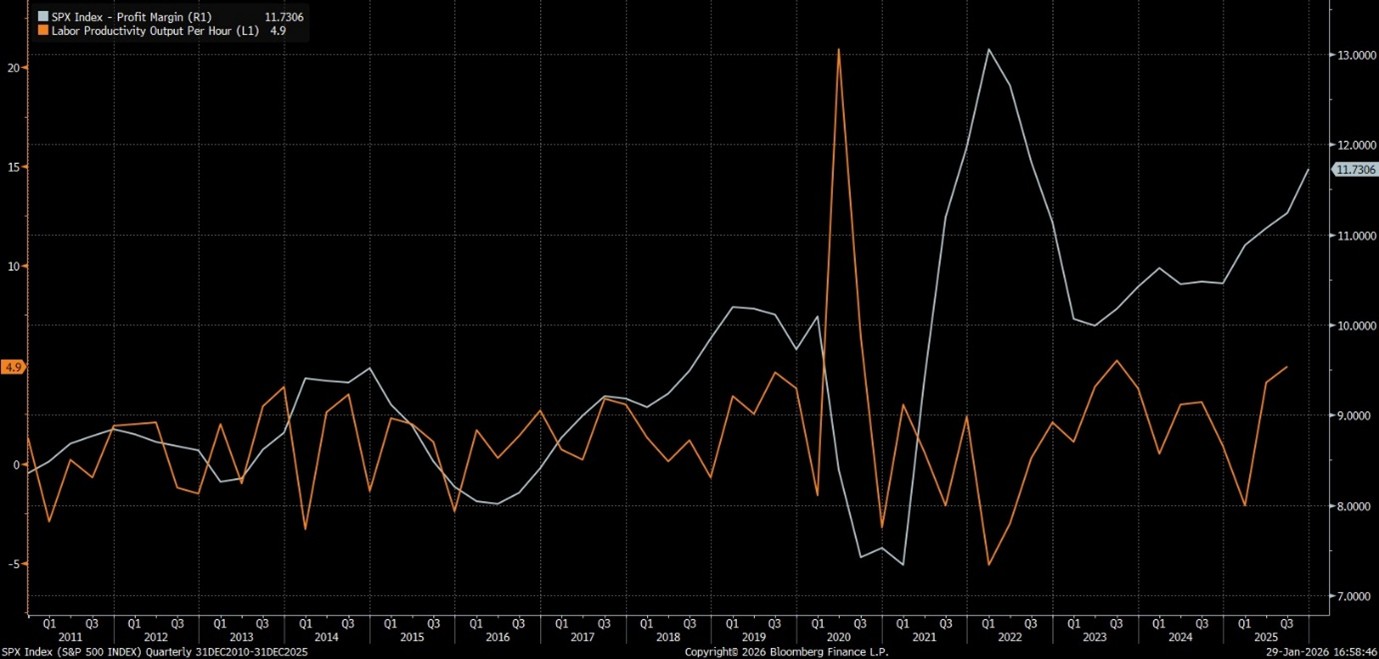

Our core view remains that corporate profit margins are on a long-term upward trajectory, supported by an imminent move upwards in labour productivity. This justifies the current massive CAPEX—not just as a "moat-building" exercise, but as a fundamental requirement for growth.

Key economic indicators that support our optimism:

- Labor Dynamics: We are observing a "hiring pause" rather than widespread firings, maintaining consumer stability.

- Manufacturing Recovery: We expect depressed ISM Manufacturing PMIs to return to levels above 50, signalling expansion.

- GDP Strength: With US GDP predicted to remain strong at 4%-6%, higher profit margins are the natural byproduct.

Notably, the banking sector continues to hit all-time highs—historically, traditional bear markets do not occur when banks are performing this well.

As long-term investors with a "low time preference" mindset, we are grappling with several key questions:

- EM Sustainability: Is the Emerging Market rally a structural shift or a temporary rerating of depressed valuations fuelled by political positioning?

- The Global Middle Point: Can challenged American allies reach a unified consensus to balance the "American Bully" stance, and how will this affect the return profiles of US-listed leaders?

- Policy Retracement: Will the pressure of midterms force the White House to soften its aggressive stance on trade and foreign policy?

Conclusion

The world is not ending; it is being rebuilt. While pundits remain fixated on the next inflation print or election poll, we remain focused on the $85 trillion buildout.

The "Software generation" provided the tools; the "Physical generation" is providing the foundation for endless abundance. The synergy between these two eras is what truly excites us. In an era of embodied intelligence and re-industrialisation, the investment opportunities seem endless. It is, quite simply, an exciting time to be an investor.