Alpine Capital Investor Newsletter - Q3 2025

Share article

1. Market Overview and Performance

The third quarter of 2025 delivered robust gains for global equities, extending the recovery from earlier-year volatility as the U.S. Federal Reserve executed its first rate cut of the cycle in September, easing to a 4.00%-4.25% range amid cooling inflation and rising unemployment concerns. This policy pivot, aligning with our prior anticipation of political pressures on the Fed to prioritise labour market stability over the elusive 2% inflation target, continued to foster a supportive environment for risk assets. Inflation has stabilised at around 3%, a level we have highlighted as a more probable baseline post-COVID and geopolitical strains. This has created a goldilocks scenario of steady growth, controlled price pressures, and accommodative monetary policy.

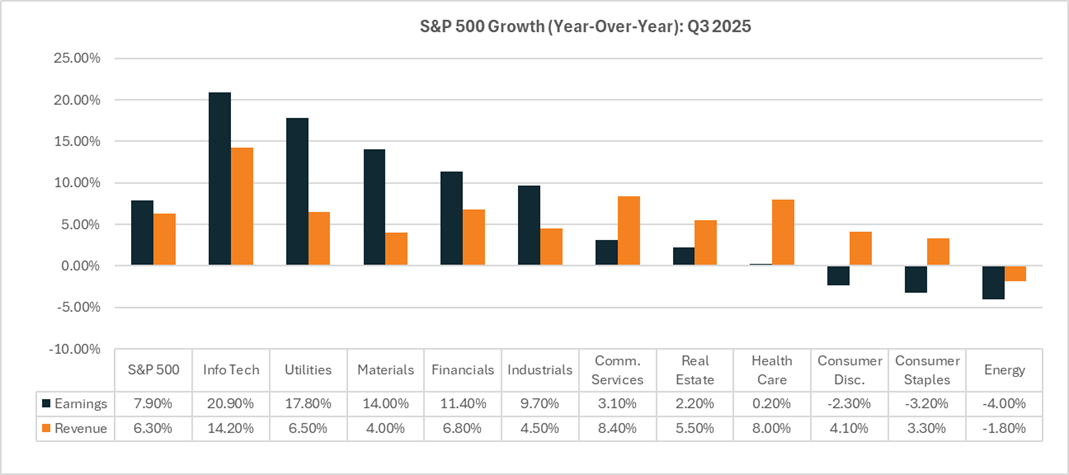

Corporate America continues to thrive, with the S&P 500 earnings outpacing expectations and underscoring resilient profitability despite bifurcation between AI-fueled tech giants and the broader economy.

The performances of the main indices have been strong over the quarter, with the MSCI All Country World Index delivering a 7.74% return, the MSCI World Index 7.37%, the S&P 500 8.11%, the Nasdaq 100 9.01%, the MSCI Emerging Markets Index 10.92%, and the JSE All Share Index 12.89%, all in US Dollar terms.

As expected, and pointed out in the Q2 newsletter, the Dollar Index seems to have found some sort of support, even if only over the short term, ending the quarter largely flat after the historic decline it endured in the first half of the year.

The South African Rand continued to strengthen against the USD, with USD/ZAR declining from approximately R17.71 in early July to around R17.27 by the end of September, a gain of approximately 2.49% for the Rand over the quarter.

2. Perspectives on AI and AI Spending

In today's fiercely competitive business landscape, organisations must prioritise investments in artificial intelligence (AI) to stave off obsolescence or severe disruption. As Larry Page reportedly stated internally at Google, "I'm willing to go bankrupt rather than lose this race", decision-makers are setting aside short-term return on investments (ROI) in favour of scaling laws that unlock emergent reasoning and inference capabilities. Don't interpret the "go bankrupt" remark literally—it's a reflection of the deep-seated fear of being left behind. Every CEO appears anxious about existential threats to their core operations, with Google, for instance, confronting a genuine challenge to its search dominance for the first time in years. This urgency is channelling spending towards AI. They simply have no choice.

Hyperscalers like Amazon, Google, and Microsoft would have invested in infrastructure regardless; AI merely redirects those funds to aligned initiatives. Efficiencies and new revenue streams will naturally emerge in due course. These mega-caps continue to outpace smaller peers across critical metrics such as returns on capital and net margins, fuelled by robust sales and earnings growth of 10%-30%. We see no signs of this momentum slowing. Such expenditures only strengthen these fundamentals, leaving us puzzled as to why investors and market commentators continue to frame it as a negative. AI promises additional upside through cost reductions and technological breakthroughs. Data centre expansions serve a dual role: displacing human labour while unlocking novel efficiencies and customer value. Much of this outlay draws from robust cash flows rather than debt, enabling sustained commitment. As we noted in the Q2 newsletter, these CAPEX levels are hardly unprecedented—absent AI, the capital would have flowed to cloud enhancements or other infrastructure spend in any event. Should returns falter in the near term, companies can pivot swiftly, as Meta Platforms did in 2022. Mark Zuckerberg's earlier wagers on underperforming ventures eroded trust and sank the stock, but a decisive shift restored investor confidence and ignited a 600%+ stock price surge over three years. The current AI spending dynamic echoes that scenario, and if it veers off course, leaders can simply halt and redirect. Backed by cash flows, this affords them tremendous agility—they can keep pace until the rhythm shifts.

Mega-caps have leveraged AI for years to enhance their ecosystems, from self-driving vehicles to warehouse automation. Emerging accelerated computing will amplify this trajectory exponentially, infusing AI across every sector. It stands to elevate efficiencies—from manufacturing floors to surgical suites—while making roadways safer, refining patient care and outcomes, and elevating global productivity. Put simply, AI holds the potential to double economic growth by empowering individuals and enterprises to achieve far more.

Concerns over an AI bubble largely centre on revenue-starved firms and startups in a winner-takes-all arena, rendering outcomes starkly binary. We approach these with caution and are steering clear for the moment. The counterargument that AI capex merely enriches players like OpenAI feels overhyped and rooted in alarmism. While short-term excesses in spending pose risks, dismissing AI's fundamental worth lacks foundation. For over a decade, investors and executives have undervalued technology's transformative potential. In this digital age, scalability knows few limits—constrained chiefly by global population rather than industrial-era bottlenecks.

That said, the circular spending within the broader semiconductor industry and OpenAI is raising some red flags, with the long-term repercussions unclear. For now, we don’t view it as a pressing crisis, and these bubble worries feel distant.

For the time being, the true beneficiaries are end consumers, who gain access to superior products and services that justify today's “elevated valuations”.

3. Reflections on Historical views & Prior decisions

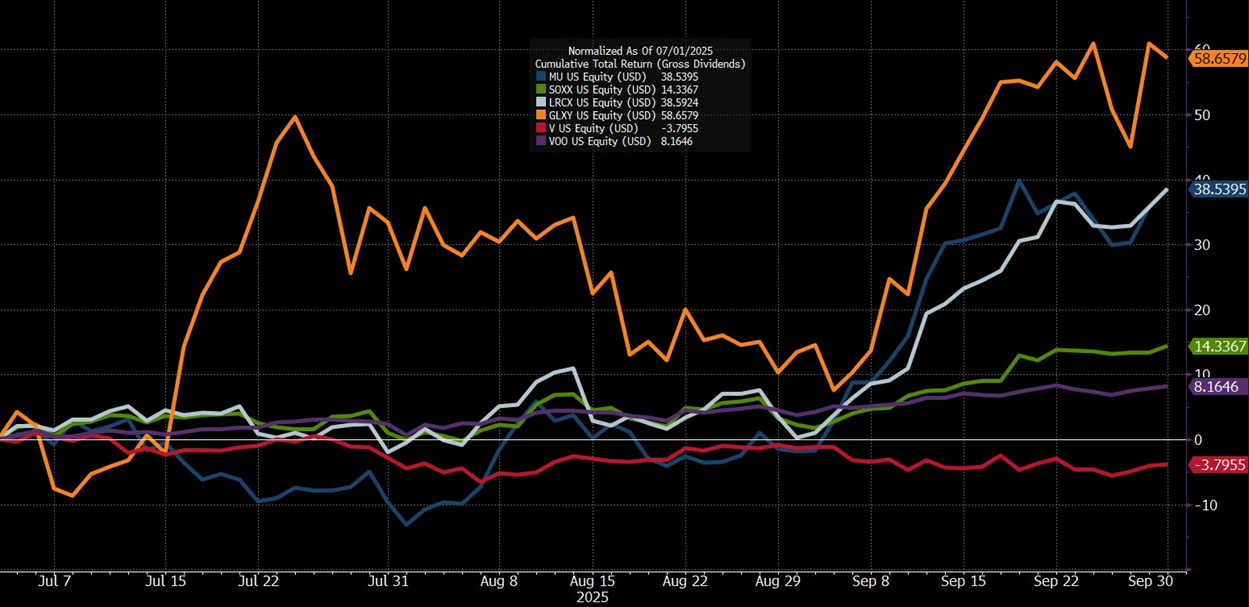

To maintain transparency, we revisit the key actions highlighted in our Q2 newsletter (available here). In our flagship Global Active Portfolio and select bespoke mandates, we executed the following:

• Sold Micron (MU) in the mid-$120s and initiated a position in the iShares Semiconductor ETF (SOXX) around $240.

• Added Lam Research (LRCX) in Q2 near $65.

• Purchased Galaxy Digital Holdings (GLXY) for around $22.50.

• Sold Visa (V) for near $350.

The accompanying chart illustrates Q3 performance for these holdings relative to the Vanguard S&P 500 ETF (VOO) benchmark (representing the S&P 500’s true returns).

While the Micron-SOXX rotation proved bittersweet as Micron extended its rally post-sale, the iShares Semiconductor ETF still outperformed the VOO benchmark, and the remaining moves all delivered positive relative returns. A satisfying outcome over this short horizon. We emphasise that short-term returns and benchmarking are secondary to our long-term discipline; it is of immense value as it sharpens our process, recognising wins and dissecting missteps alike.

Beyond adding gold to our ETF portfolios, we held steady on purpose this quarter. In a choppy market, it might seem like we're just sitting tight, but that's really about staying sharp: constantly sizing up new ideas and passing on those that don't quite align with our core strategy.

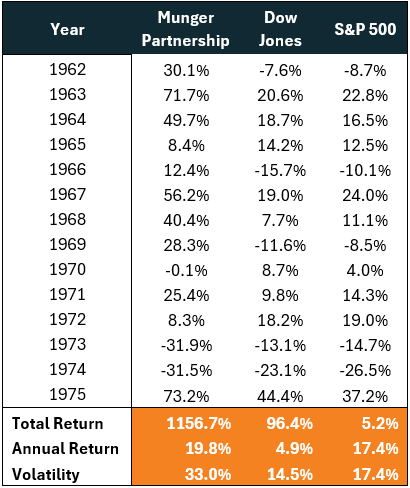

This "active inaction" demands effort—researching prospects, stress-testing ideas, and resisting the urge to make changes for the sake of making changes. We remain convinced that concentrated, low-turnover portfolios offer the clearest path to outperformance, provided investors embrace volatility that is higher than the benchmark. Consider Charlie Munger's early partnership, where volatility was close to 2x the market's, yet compounded to superior results. The table below captures this dynamic from 1962–1975.

In short, we trust our process and need to give the underlying companies and management teams we back a fair chance: if you've done the groundwork and stand by the thesis that drew you in, volatility becomes noise.

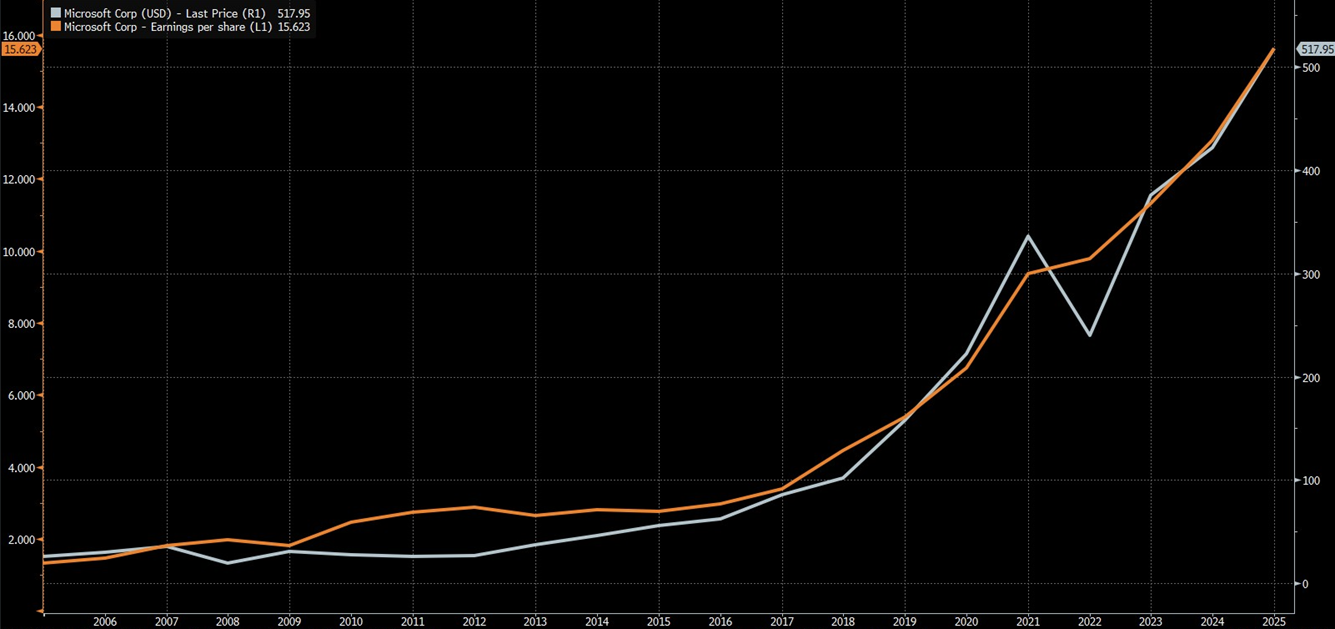

Over time, share prices align with earnings power—as Microsoft's long-term chart illustrates below.

4. Outlook

The Fed's next moves appear all but assured: two 25bps cuts this year, in late October and December, with the first locked in and the second highly probable.

The US Fed’s rate policy remains the most important indicator in trying to predict global asset class returns. We’ve seen a clear pivot from a focus on inflation to a focus on the labour market—in other words, inflation is not at the forefront anymore, and the 2% target seems to have shifted to the 3% region.

This current rate-easing cycle—underpinned by 3.8% GDP growth, 7% U.S. fiscal deficits, as well as supportive policy—renders structural bearishness and a large-scale sell-off unlikely. For now, upside momentum endures; sharp selloffs will demand extraordinary triggers, like intensifying U.S.-China frictions that lead to actual political and economic fallouts.

On the local front, should commodity tailwinds persist, the Rand and JSE should hold firm. We do, however, caution against continued lofty expectations of endless continuity—South Africa's economy remains deeply concentrated in cyclical commodities, alongside banks and Naspers/Prosus, while grappling with entrenched political and structural headwinds.

At the start of 2025, we anticipated modest gains from equities. So far, results have quietly exceeded those expectations. But we're not getting carried away—markets are notoriously hard to predict, and we hold onto our overarching thesis that strong, genuine, real returns are the reward for those who stick around for the long term. The system favours patient investors, and we're excellently positioned to continue reaping those benefits.